시장 개관

| 학습 기간 | 2017 - 2030 |

| 산정기준연도 | 2024 |

| 예측 데이터 기간 | 2025 - 2030 |

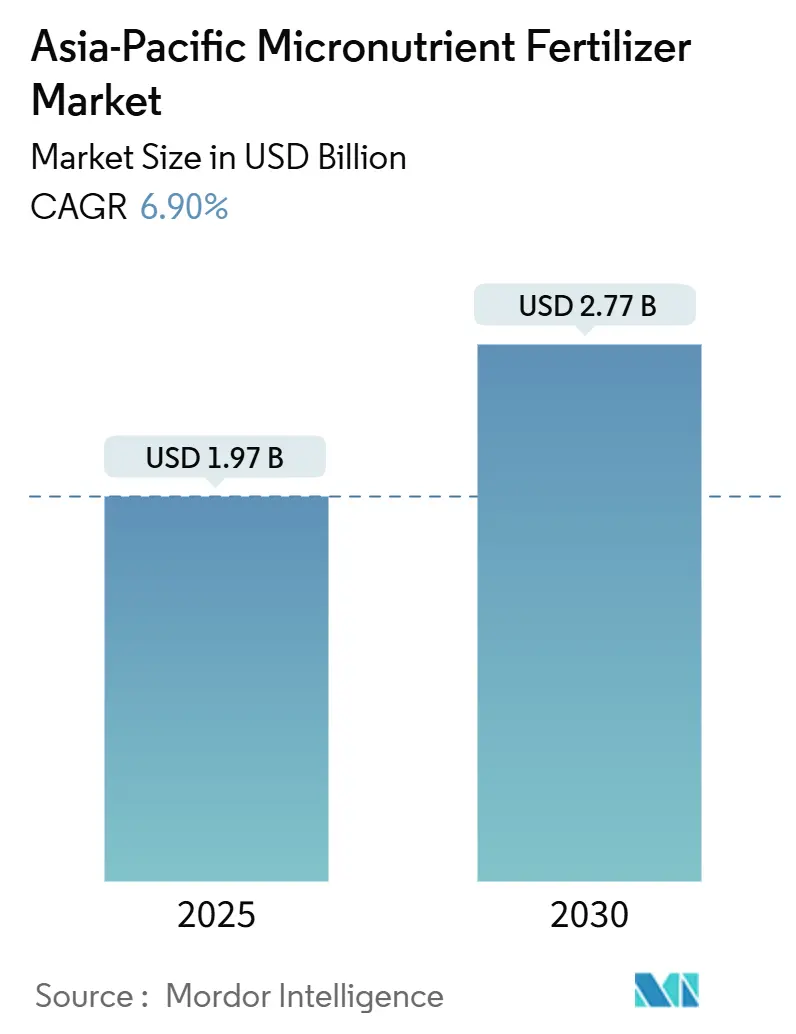

| 시장 규모(2025년) | USD 1.97 십억 |

| 시장 규모(2030년) | USD 2.77 십억 |

| 성장률(2025년~2030년) | 6.90 % CAGR |

| 시장 집중 | 높음 |

주요 선수*면책조항: 주요 플레이어는 특별한 순서 없이 정렬되었습니다. 이미지 © 바카라 사이트. 재사용 시 CC BY 4.0에 따라 저작자 표시가 필요합니다. |

|

Asia-Pacific Micronutrient Fertilizer Market Analysis by 바카라 사이트

The Asia-Pacific micronutrient fertilizer market size is valued at USD 1.97 billion in 2025 and is forecast to reach USD 2.77 billion in 2030, advancing at a 6.9% CAGR during 2025-2030. The upward trajectory reflects expanding precision-farming practices, widespread micronutrient deficiencies, and supportive fiscal incentives that lower input costs for smallholders. Province-level zinc subsidies in China also buoy the Asia-Pacific micronutrient fertilizer market, GST reductions in India, and fertigation uptake in Australia, all of which widen product access, spur demand for specialized formulations, and create white-space opportunities for regional innovators. Heightened digital-platform penetration, led by BASF’s xarvio and India’s Geoagro-iKrishi, accelerates advisory reach, while supply-side advances in nano and chelated technologies improve nutrient-use efficiency. However, raw-material price volatility for zinc sulfate ores, limited rural credit in parts of South Asia, and an influx of counterfeit inputs in Indonesia and the Philippines introduce short-term headwinds that temper but do not derail overall expansion of the Asia-Pacific micronutrient fertilizer market.

주요 바카라 요약

- By product category, copper held 32.1% of the Asia-Pacific micronutrient fertilizer market share in 2024, while boron is projected to expand at an 8.1% CAGR through 2030.

- By application mode, soil application accounted for a 96.3% share of the Asia-Pacific micronutrient fertilizer market size in 2024 and fertigation is advancing at a 7.4% CAGR to 2030.

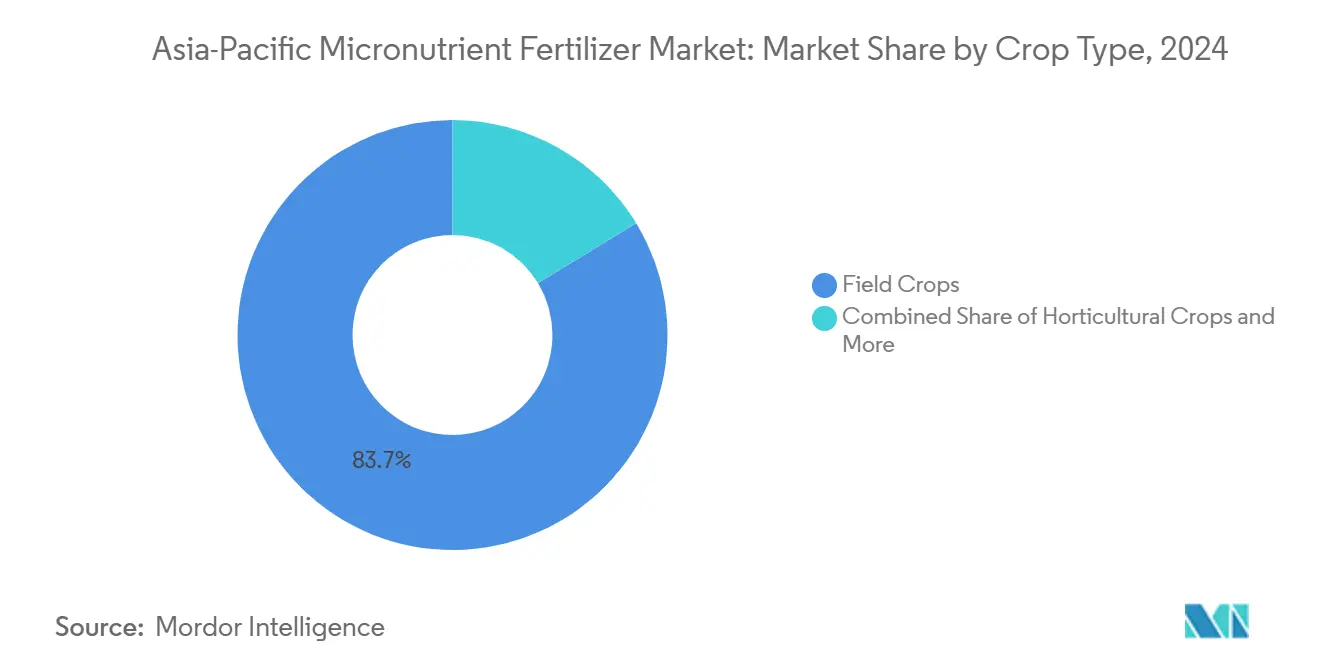

- By crop type, field crops commanded 83.7% of the Asia-Pacific micronutrient fertilizer market size in 2024, turf and ornamental crops are forecast to grow at a 9.0% CAGR through 2030.

- By geography, India led with a 41.4% Asia-Pacific micronutrient fertilizer market share in 2024, whereas Australia records the highest projected CAGR at 8.7% to 2030.

Asia-Pacific Micronutrient Fertilizer Market Trends and Insights

드라이버 영향 분석

| 운전기사 | (~) CAGR 예측에 미치는 영향 | 지리적 관련성 | 영향 타임라인 |

|---|---|---|---|

| China's Zinc Subsidies Target Hidden Hunger Crisis | 1.2% | China core, spillover to wider Asia-Pacific | 중기(2~4년) |

| Australia's Fertigation Revolution in Protected Horticulture | 0.8% | Australia, New Zealand, spreading to Southeast Asia | 단기 (≤ 2년) |

| India's Soil Health Cards Drive Systematic Micronutrient Testing | 1.5% | India core, replication in Bangladesh and Pakistan | 장기 (≥ 4년) |

| Digital Platforms Accelerate Precision Micronutrient Applications | 0.7% | Vietnam, Thailand, widening to the Philippines | 중기(2~4년) |

| Specialty-Crop Expansion Drives Customized Demand | 0.9% | Region-wide, strongest in India and China | 단기 (≤ 2년) |

| Consumer Demand for Fortified Foods Spurs Farm-Level Biofortification | 0.6% | Major rice-growing areas of Asia-Pacific | 장기 (≥ 4년) |

출처: 모르도르 정보

이 시장을 형성하는 주요 추세 이해

PDF 다운로드

China's Zinc Subsidies Target Hidden Hunger Crisis

China’s nutrition-centric subsidy scheme reallocates provincial funds toward zinc-enriched fertilizers that lift grain micronutrient density instead of merely boosting yields. The initiative reframes product success metrics around grain zinc content and aligns public health goals with farm-level practices, pushing the Asia-Pacific micronutrient fertilizer market toward value-added formulations. Field evidence shows foliar zinc delivers 55.2% higher biofortification efficacy than soil application, spurring R&D into next-generation foliar sprays. Multiplier effects arise as neighboring countries monitor China’s program to replicate its public health gains, unlocking additional addressable demand for specialized suppliers.

Australia's Fertigation Revolution in Protected Horticulture

Water-scarce Australia prioritizes fertigation to minimize waste and fine-tune nutrient timing for high-density blueberries and other greenhouse fruit crops[1]Source: Australian Government Department of Agriculture, “Protected Horticulture Industry Analysis,” agriculture.gov.au. This shift favors fully water-soluble chelated micronutrients that command premium pricing yet deliver measurable yield-and-quality gains. Early adopters report reductions in iron chlorosis episodes and improved firmness in export berries, catalyzing copy-cat investments in New Zealand and Southeast Asian greenhouses. Rising fertigation acreage, therefore, underwrites the fastest-growing application segment of the Asia-Pacific micronutrient fertilizer market.

Digital Platforms Accelerate Precision Micronutrient Applications

Platforms such as BASF’s xarvio and IRRI’s Rice Crop Manager blend satellite imagery, local weather, and soil analytics to dispense field-specific dosage alerts. These channels bypass legacy distribution layers, curbing counterfeit infiltration and enabling vendors to bundle premium chelated or nano products with agronomic support. Larger datasets continuously refine algorithms, improving recommendation accuracy and farmer trust, which in turn elevates adoption rates in the Asia-Pacific micronutrient fertilizer market.

Specialty-Crop Expansion Drives Customized Demand

Vietnam’s avocado plantings and Thailand’s blueberry acreage draw attention to boron-mediated fruit set and copper-dependent disease management, respectively. Because export buyers enforce strict nutrient specifications, growers willingly pay for crop-specific blends, encouraging manufacturers to differentiate SKUs by phenological stage and soil pH. Such diversification grows the value pool even if total micronutrient metric tons remain modest, reinforcing boron’s status as the fastest-growing product.

제약 영향 분석

| 제지 | (~) CAGR 예측에 미치는 영향 | 지리적 관련성 | 영향 타임라인 |

|---|---|---|---|

| Raw-Material Price Volatility Constrains Market Accessibility | -1.1 % | China, Australia, wider Asia-Pacific | 단기 (≤ 2년) |

| Credit Constraints Limit Premium Product Adoption | -0.8 % | Bangladesh, Pakistan, rural India | 중기(2~4년) |

| Counterfeit Products Erode Farmer Confidence | -0.6 % | 인도네시아, 필리핀, 베트남 | 중기(2~4년) |

| Port Bottlenecks Delay Chelated Micronutrient Exports | -0.4 % | China export-dependent markets | 단기 (≤ 2년) |

출처: 모르도르 정보

Raw-Material Price Volatility Constrains Market Accessibility

China’s mine closures under stringent environmental mandates curtail the supply of high-grade zinc sulfate ores, lifting feedstock costs and cascading into micronutrient price swings. Distributors struggle to hedge inventories, forcing periodic price hikes that strain smallholders’ cash flow and hinder uptake. Chelated and nano formulations, which rely on purer inputs, bear disproportionate cost pressure, narrowing the adoption of these high-efficacy options within the Asia-Pacific micronutrient fertilizer market.

Credit Constraints Limit Premium Product Adoption

In Bangladesh, where 80% of fertilizers are imported, currency volatility inflates landed costs and stretches subsidy budgets. Commercial banks in Pakistan apply conservative lending norms, preferring to finance low-risk NPK purchases. Without affordable seasonal credit, smallholders postpone or skip micronutrient applications despite proven yield benefits, muting the Asia-Pacific micronutrient fertilizer market’s value potential in lower-income segments.

세그먼트 분석

By Product: Copper Resilience Meets Boron Upswing

Copper dominated the Asia-Pacific micronutrient fertilizer market with a 32.1% share in 2024, driven by its longstanding use in rice systems and dual agronomic-fungicidal role. The segment’s entrenched distributor networks and field-trial familiarity underpin stable volume even as chelated alternatives emerge. Boron, however, is on track to post an 8.1% CAGR to 2030 as fruit-crop acreage expands in Southeast Asia, foliar boron applications have lifted citrus fruit set by up to 25%. Producers leverage differentiated packaging and crop-stage labeling to convert grower awareness into repeat purchases, reinforcing the Asia-Pacific micronutrient fertilizer market size outlook. Product portfolios now feature soluble boron for fertigation and controlled-release boron for sandy soils, ensuring relevance across diverse agro-ecologies.

Continued R&D in nano copper seeks to curtail phytotoxicity and enhance uptake, a move anticipated to preserve copper’s revenue base even as regulatory scrutiny over heavy-metal accumulation tightens. Zinc remains buoyed by policy support, while iron sees heightened closed-system demand in hydroponics. Emerging nutrients such as selenium appear in specialty blends targeting niche deficiencies. Collectively, such diversification ensures that the Asia-Pacific micronutrient fertilizer market retains a balanced mix of high-volume staples and high-value innovations.

참고: 바카라 구매 시 사용 가능한 모든 개별 세그먼트의 세그먼트 공유

By Application Mode: Soil Dominance but Fertigation Momentum

Soil broadcasting held 96.3% of the Asia-Pacific micronutrient fertilizer market size in 2024 because broad-acre rice, wheat, and corn rely on inexpensive granular formulations applied with existing spreaders. Yet fertigation is slated to deliver a 7.4% CAGR through 2030 as water-efficient protected cultivation gains ground. Growers deploying drip lines in Australian berry tunnels report tighter pH control and higher iron uptake, validating fertigation’s agronomic edge. Suppliers thus prioritize fully soluble chelates packaged in 1-kilogram foil sachets that dissolve instantly in irrigation tanks.

Foliar spraying remains a tactical option for in-season correction and biofortification programs, particularly during reproductive stages when nutrient translocation into grain is critical. While labor-intensive, foliar usage commands premium prices and embeds services such as tissue testing. Integration of sensors and sectional control nozzles further optimizes droplet placement, boosting return on investment and sustaining the Asia-Pacific micronutrient fertilizer market’s technological narrative.

By Crop Type: Field-Crop Stability Set Against Ornamental Upside

Field crops anchored 83.7% of Asia-Pacific micronutrient fertilizer market share in 2024, reflecting the vast 60 million-hectare rice footprint plus wheat and maize acreage concentrated in India and China. State procurement programs and staple-food security imperatives preserve this volume base. Nonetheless, turf and ornamental demand is expanding at a 9.0% CAGR, propelled by municipal landscaping and golf-course builds across urbanizing Association of Southeast Asian Nations (ASEAN) economies. These end-users favor homogenous micro-granules and slow-release coatings that deliver aesthetic benefits and reduce scorch risk.

Horticultural crops sit between the two extremes, registering steady uptake as middle-class diets shift toward fruit and vegetables. Export-oriented growers in Vietnam adhere to stringent residue limits, incentivizing micronutrient use to meet cosmetic standards without boosting synthetic pesticide applications. This balanced demand profile supports resilient revenue expansion for the Asia-Pacific micronutrient fertilizer market.

참고: 바카라 구매 시 사용 가능한 모든 개별 세그먼트의 세그먼트 공유

지리 분석

India anchors the Asia-Pacific micronutrient fertilizer market with a 41.4% share, propelled by 247.4 million Soil Health Cards that spotlight zinc and iron gaps across varied agro-climatic zones[2]Source: Ministry of Agriculture and Farmers Welfare, “Soil Health Card Portal,” soilhealth.dac.gov.in. Lower GST and domestic nano-fertilizer output by IFFCO enhance affordability, while the Geoagro-iKrishi app pushes real-time recommendations to 2 million growers. As a result, micronutrient adoption among smallholders has risen markedly since 2024, reinforcing India’s leadership position.

China contributes a sizable volume through nutrition-focused subsidies that reposition zinc as a public-health input rather than a yield enhancer, aligning agricultural and health ministries toward common goals[3]Source: Nature Publishing Group, “Global Zinc Deficiency Prevalence Study,” nature.com. However, environmental curbs on mining and stricter port checks inject periodic volatility into export flows, compelling downstream players to diversify sourcing. The internal push toward digital farming platforms further refines demand forecasting, benefiting data-integrated suppliers.

Australia delivers the region’s fastest growth, accounting for 8.7% CAGR as protected horticulture acreage widens. Drip-fed blueberry tunnels and high-value greenhouse tomatoes adopt chelated blends that minimize precipitation at alkaline pH, supporting premium price realization. Elsewhere, Bangladesh and Pakistan work to alleviate credit bottlenecks, whereas Indonesia and the Philippines invest in anti-counterfeit enforcement. Combined, these markets provide incremental upside that helps the Asia-Pacific micronutrient fertilizer market achieve its forecast CAGR.

중요한 지리적 시장에 대한 분석을 받아보세요

PDF 다운로드

경쟁 구도

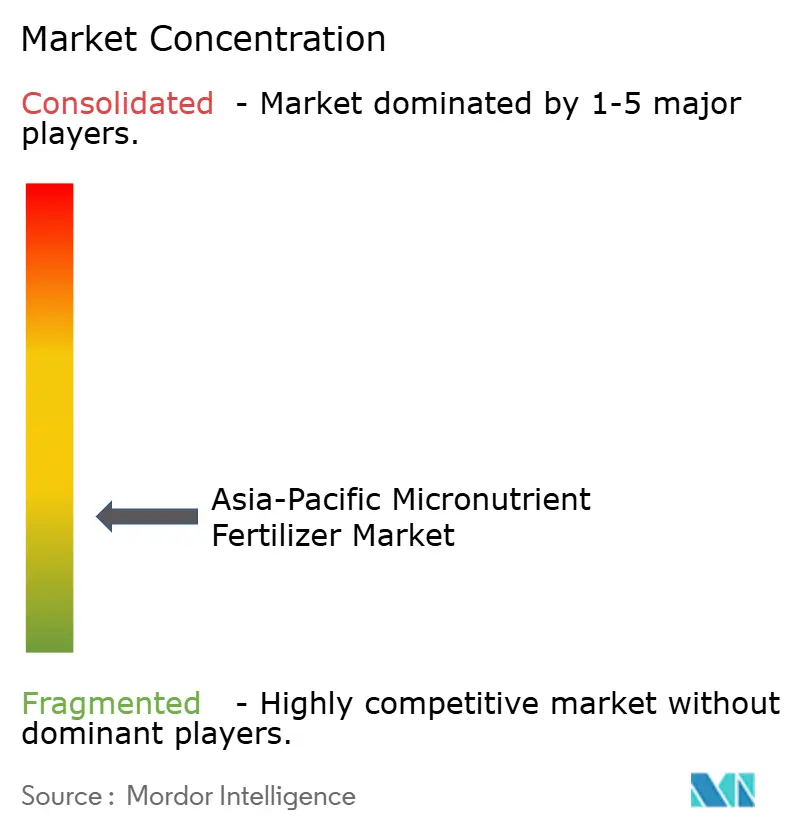

The Asia-Pacific micronutrient fertilizer market exhibits fragmented competition, with the top 5 players controlling a significant market share, creating substantial opportunities for regional specialists and technology innovators to capture market segments through differentiated product offerings and localized distribution strategies. This fragmentation reflects diverse agricultural systems, varying regulatory frameworks, and distinct crop requirements across the region that prevent any single player from achieving dominant market control.

Competition intensity centers on product innovation, particularly in nano-formulations and chelated micronutrients that offer superior bioavailability and application convenience compared to traditional sulfate-based products. Strategic patterns emphasize vertical integration and technology partnerships, with companies like IFFCO developing nano urea plus production capacity of 17 crore bottles annually, while maintaining extensive cooperative distribution networks that reach smallholder farmers directly.

Digital agriculture integration represents a key competitive differentiator, as companies partner with platform providers to deliver precision recommendations that optimize micronutrient applications based on soil testing data and crop monitoring insights. White-space opportunities exist in specialty crop segments, biofortification applications, and emerging markets where agricultural modernization creates demand for advanced micronutrient solutions. The competitive landscape benefits from regulatory frameworks established by bodies like Japan's FAMIC (Food and Agricultural Materials Inspection Center), which ensures product quality standards that support market development and farmer confidence in micronutrient investments.

Asia-Pacific Micronutrient Fertilizer Industry Leaders

-

참발 무료 바카라 게임 및 화학 회사

-

코로만델인터내셔널

-

인도 농민 무료 바카라 게임 협동 조합 제한

-

야라 인터내셔널 ASA

-

Zuari 농업 화학 주식 회사

- *면책조항: 주요 플레이어는 특별한 순서 없이 정렬되었습니다.

시장 참가자 및 경쟁사에 대한 자세한 정보가 필요하십니까?

PDF 다운로드

최근 산업 발전

- November 2024: Nutrien Ag Solutions has initiated construction on a new USD 70 million distribution center. This larger facility will boost the company's storage capacity for bulk granular fertilizers, including micronutrient fertilizers, by 20%, bringing the total to 130,000 Metric tons.

- May 2024: iffco revealed that the central government greenlit the launch of its two new offerings including nano liquid zinc and nano liquid copper. These innovations aim to address zinc and copper deficiencies in agricultural crops, thereby enhancing productivity.

- May 2023: Yara International announced plans for a new production facility in Yorkshire, UK, focused on specialty crop nutrition products and biostimulants to boost yields and quality. Expected to be operational by late 2025, the plant will double YaraVita production capacity, with potential for further expansion. Nearly all output will be exported to markets around the world, strengthening Yara's micronutrient fertilizer production.

이 바카라를 사용하면 무료

바카라와 함께 우리는 재배 면적과 헥타르당 평균 적용률에 대한 25개 이상의 그래프가 포함된 포괄적이고 철저한 데이터 팩도 제공합니다. 데이터 팩에는 글로브, 북미, 유럽, 아시아 태평양, 남미 및 아프리카가 포함됩니다.

표 및 그림 목록

- 그림 1 :

- 2017년부터 2022년까지 아시아 태평양 지역 헥타르 규모의 농작물 재배

- 그림 2 :

- 아시아 태평양 지역 원예 작물 재배(2017~2022년)

- 그림 3 :

- 2022년 아시아 태평양 밭작물별 미량 영양소 소비량(KG/헥타르)

- 그림 4 :

- 2022년 아시아 태평양 원예 작물의 미량 영양소 소비량(KG/헥타르)

- 그림 5 :

- 2022년 아시아 태평양 헥타르의 관개 시설을 갖춘 농업 토지

- 그림 6 :

- 2017년부터 2030년까지 아시아 태평양 지역의 미량 영양소 무료 바카라 게임 소비량(미터톤)

- 그림 7 :

- 2017년부터 2030년까지 아시아 태평양의 미량 영양소 무료 바카라 게임 소비량(미국 달러)

- 그림 8 :

- 아시아 태평양(2017~2030년), 미터톤(미터톤) 기준 제품별 미량 영양소 무료 바카라 게임 소비량

- 그림 9 :

- 아시아 태평양, 2017년 - 2030년, 미국 달러 기준 미량 영양소 무료 바카라 게임 소비량

- 그림 10 :

- 제품별 미량 영양소 무료 바카라 게임 소비량(%), 아시아 태평양, 2017 VS 2023 VS 2030

- 그림 11 :

- 제품별 미량 영양소 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2017년 VS 2023년 VS 2030년

- 그림 12 :

- 아시아 태평양 미터톤당 붕소 무료 바카라 게임 소비량(2017~2030년)

- 그림 13 :

- 2017년부터 2030년까지 아시아 태평양의 붕소 무료 바카라 게임 소비량(USD)

- 그림 14 :

- 작물 유형별 붕소 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 15 :

- 미터톤당 구리 무료 바카라 게임 소비량, 아시아 태평양, 2017년 - 2030년

- 그림 16 :

- 2017년부터 2030년까지 아시아 태평양의 구리 무료 바카라 게임 소비량(미국 달러)

- 그림 17 :

- 작물 유형별 구리 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 18 :

- 아시아 태평양 미터톤의 철 무료 바카라 게임 소비량(2017~2030년)

- 그림 19 :

- 2017년부터 2030년까지 아시아 태평양의 철 무료 바카라 게임 소비량(미국 달러 기준)

- 그림 20 :

- 작물 유형별 철 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 21 :

- 아시아 태평양 미터톤당 망간 무료 바카라 게임 소비량(2017~2030년)

- 그림 22 :

- 2017년 - 2030년 아시아 태평양의 망간 무료 바카라 게임 소비량(미국 달러)

- 그림 23 :

- 작물 유형별 망간 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 24 :

- 아시아 태평양, 2017년 - 2030년 미터톤당 몰리브덴 무료 바카라 게임 소비량

- 그림 25 :

- 2017년 - 2030년 아시아 태평양 몰리브덴 무료 바카라 게임 소비량(미국 달러)

- 그림 26 :

- 작물 유형별 몰리브덴 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 27 :

- 아시아 태평양 미터톤 기준 아연 무료 바카라 게임 소비량(2017~2030년)

- 그림 28 :

- 2017년 - 2030년 아시아 태평양의 아연 무료 바카라 게임 소비량(USD)

- 그림 29 :

- 작물 유형별 아연 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 30 :

- 기타 무료 바카라 게임 소비량(미터톤, 아시아 태평양, 2017~2030년)

- 그림 31 :

- 기타 무료 바카라 게임 소비량(미국 달러, 아시아 태평양, 2017~2030)

- 그림 32 :

- 기타 작물 유형별 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 33 :

- 미량 영양소 미량 영양소 아시아 태평양 지역의 적용 모드별 무료 바카라 게임 소비량(미터톤), 2017-2030

- 그림 34 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비량 (미국 달러 기준), 아시아 태평양, 2017-2030

- 그림 35 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비량(적용 모드별) (%, 아시아 태평양, 2017년 대비 2023년 대비 2030년)

- 그림 36 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비 가치(적용 모드별)(%, 아시아 태평양, 2017년 대비 2023년 대비 2030년)

- 그림 37 :

- 미터톤의 미량 영양소 무료 바카라 게임 시비, 아시아 태평양, 2017년 - 2030년

- 그림 38 :

- 아시아 태평양, 2017년 - 2030년 미국 달러 기준 미량 영양소 무료 바카라 게임의 시비 적용

- 그림 39 :

- 농작물 유형별 미량 영양소 무료 바카라 게임 시비(%), 아시아 태평양, 2023년 VS 2030년

- 그림 40 :

- 아시아 태평양 미터톤의 미량 영양소 무료 바카라 게임의 엽면 살포(2017~2030년)

- 그림 41 :

- 아시아 태평양, 2017년~2030년 미국 달러 기준 미량 영양소 무료 바카라 게임의 엽면 살포

- 그림 42 :

- 작물 유형별 미량 영양소 무료 바카라 게임의 엽면 살포 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 43 :

- 미터톤(미터톤)의 미량 영양소 무료 바카라 게임의 토양 시용, 아시아 태평양, 2017년 - 2030년

- 그림 44 :

- 아시아 태평양(2017~2030년) 미달러 기준 미량 영양소 무료 바카라 게임의 토양 시비

- 그림 45 :

- 작물 유형별 미량 영양소 무료 바카라 게임의 토양 시용 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 46 :

- 미량 영양소 미량 영양소 작물 유형별 무료 바카라 게임 소비량(미터톤), 아시아 태평양, 2017-2030

- 그림 47 :

- 미량 영양소 미량 영양소 작물 유형별 무료 바카라 게임 소비량(USD), 아시아 태평양, 2017-2030

- 그림 48 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비량(작물 유형별) (%, 아시아 태평양, 2017년 대비 2023년 대비 2030년)

- 그림 49 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비 가치 작물 유형별 %, 아시아 태평양, 2017년 대비 2023년 대비 2030년

- 그림 50 :

- 아시아 태평양, 2017년부터 2030년까지 밭 작물별 미량 영양소 무료 바카라 게임 소비량(미터톤)

- 그림 51 :

- 아시아 태평양, 2017~2030년 농작물별 미량 영양소 무료 바카라 게임 소비량(미국 달러 기준)

- 그림 52 :

- 제품별 미량 영양소 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 53 :

- 2017년부터 2030년까지 아시아 태평양, 미터톤(미터톤) 기준 원예 작물별 미량 영양소 무료 바카라 게임 소비량

- 그림 54 :

- 아시아 태평양, 2017~2030년 원예 작물별 미량 영양소 무료 바카라 게임 소비(미국 달러 기준)

- 그림 55 :

- 제품별 미량 영양소 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 56 :

- 아시아 태평양, 2017년 - 2030년 미터톤 기준 잔디 및 관상용 미량 영양소 무료 바카라 게임 소비량

- 그림 57 :

- 아시아 태평양, 2017~2030년 잔디 및 장식용 미량 영양소 무료 바카라 게임 소비량(미국 달러 기준)

- 그림 58 :

- 제품별 미량 영양소 무료 바카라 게임 소비 가치(%), 아시아 태평양, 2023년 VS 2030년

- 그림 59 :

- 미량 영양소 미량 영양소 아시아 태평양 국가별 무료 바카라 게임 소비량(미터톤), 2017-2030

- 그림 60 :

- 미량 영양소 미량 영양소 국가별 무료 바카라 게임 소비량(달러), 아시아 태평양, 2017-2030

- 그림 61 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비량(국가별, %, 아시아 태평양, 2017년 대비 2023년 대비 2030년)

- 그림 62 :

- 미량 영양소 미량 영양소 무료 바카라 게임 소비 가치 국가별 %, 아시아 태평양, 2017년 대비 2023년 대비 2030년

- 그림 63 :

- 2017년부터 2030년까지 호주, 미터톤 단위의 미량 영양소 무료 바카라 게임 소비량

- 그림 64 :

- 미량 영양소 무료 바카라 게임 소비량(미국 달러, 호주, 2017년 - 2030년)

- 그림 65 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 호주, 2023년 VS 2030년

- 그림 66 :

- 2017년부터 2030년까지 방글라데시 미터톤의 미량 영양소 무료 바카라 게임 소비량

- 그림 67 :

- 미량 영양소 무료 바카라 게임 소비량(USD, 방글라데시, 2017-2030)

- 그림 68 :

- 농작물 종류별 미량 영양소 무료 바카라 게임 소비량(%), 방글라데시, 2023년 VS 2030년

- 그림 69 :

- 2017년부터 2030년까지 중국 미터톤의 미량 영양소 무료 바카라 게임 소비량

- 그림 70 :

- 2017년부터 2030년까지 중국의 미량 영양소 무료 바카라 게임 소비량(미국 달러)

- 그림 71 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 중국, 2023년 VS 2030년

- 그림 72 :

- 2017년부터 2030년까지 인도, 미터톤 단위의 미량 영양소 무료 바카라 게임 소비량

- 그림 73 :

- 미량 영양소 무료 바카라 게임 소비량(미국 달러, 인도, 2017~2030년)

- 그림 74 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 인도, 2023년 VS 2030년

- 그림 75 :

- 2017년부터 2030년까지 인도네시아, 미터톤 단위의 미량 영양소 무료 바카라 게임 소비량

- 그림 76 :

- 미량 영양소 무료 바카라 게임 소비량(USD, 인도네시아, 2017~2030)

- 그림 77 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 인도네시아, 2023년 VS 2030년

- 그림 78 :

- 2017년부터 2030년까지 일본 미터톤의 미량 영양소 무료 바카라 게임 소비량

- 그림 79 :

- 2017년부터 2030년까지 일본의 미량 영양소 무료 바카라 게임 소비량(미국 달러 기준)

- 그림 80 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 일본, 2023년 VS 2030년

- 그림 81 :

- 2017년부터 2030년까지 파키스탄, 미터톤 단위의 미량 영양소 무료 바카라 게임 소비량

- 그림 82 :

- 2017년부터 2030년까지 파키스탄의 미량 영양소 무료 바카라 게임 소비량(USD)

- 그림 83 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 파키스탄, 2023년 VS 2030년

- 그림 84 :

- 2017년부터 2030년까지 필리핀의 미터톤당 미량 영양소 무료 바카라 게임 소비량

- 그림 85 :

- 2017년부터 2030년까지 필리핀의 미량 영양소 무료 바카라 게임 소비량(미국 달러)

- 그림 86 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 필리핀, 2023년 VS 2030년

- 그림 87 :

- 2017년 - 2030년 태국 미터톤 기준 미량 영양소 무료 바카라 게임 소비량

- 그림 88 :

- 2017년 - 2030년 태국 미화 영양소 무료 바카라 게임 소비량

- 그림 89 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 태국, 2023년 VS 2030년

- 그림 90 :

- 2017년부터 2030년까지 베트남 미터톤의 미량 영양소 무료 바카라 게임 소비량

- 그림 91 :

- 2017년부터 2030년까지 베트남의 미량 영양소 무료 바카라 게임 소비량(USD)

- 그림 92 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비 가치(%), 베트남, 2023년 VS 2030년

- 그림 93 :

- 미량 영양소 무료 바카라 게임 소비량(미터톤), 기타 아시아 태평양 지역, 2017년 - 2030년

- 그림 94 :

- 2017년 - 2030년, 기타 아시아 태평양 지역의 미량 영양소 무료 바카라 게임 소비량(미국 달러)

- 그림 95 :

- 작물 유형별 미량 영양소 무료 바카라 게임 소비량(%), 기타 아시아 태평양 지역, 2023년 VS 2030년

- 그림 96 :

- 2017~2030년 아시아 태평양 지역의 전략적 움직임 수 기준 가장 활동적인 기업

- 그림 97 :

- 아시아 태평양 미량 영양소 무료 바카라 게임 시장, 가장 많이 채택된 전략, 2018-2021

- 그림 98 :

- 주요 기업의 시장 점유율(%, 아시아 태평양)

Asia-Pacific Micronutrient Fertilizer Market Report Scope

붕소, 구리, 철, 망간, 몰리브덴, 아연, 기타는 제품별로 세그먼트로 다룹니다. 시비, 잎, 토양은 적용 모드별로 세그먼트로 다룹니다. 밭 작물, 원예 작물, 잔디 및 관상용 작물은 작물 유형별로 세그먼트로 다룹니다. 호주, 방글라데시, 중국, 인도, 인도네시아, 일본, 파키스탄, 필리핀, 태국, 베트남은 국가별로 세그먼트로 다룹니다.| 프로덕트 | 붕소 |

| 구리 | |

| 철 | |

| 망간 | |

| 몰리브덴 | |

| 아연 | |

| 기타 | |

| 응용 모드 | 비료 |

| 잎 | |

| 흙 | |

| 자르기 유형 | 들판 작물 |

| 원예 작물 | |

| 잔디 및 관상용 | |

| 지리학 | Australia |

| 방글라데시 | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| 파키스탄 | |

| Philippines | |

| Thailand | |

| Vietnam | |

| 아시아 태평양 기타 지역 |

프로덕트

| 붕소 |

| 구리 |

| 철 |

| 망간 |

| 몰리브덴 |

| 아연 |

| 기타 |

응용 모드

| 비료 |

| 잎 |

| 흙 |

자르기 유형

| 들판 작물 |

| 원예 작물 |

| 잔디 및 관상용 |

지리학

| Australia |

| 방글라데시 |

| China |

| India |

| Indonesia |

| Japan |

| 파키스탄 |

| Philippines |

| Thailand |

| Vietnam |

| 아시아 태평양 기타 지역 |

다른 지역이나 세그먼트가 필요하신가요?

지금 사용자 정의

시장 정의

- 시장 추정 수준 - 다양한 유형의 무료 바카라 게임에 대한 시장 추정은 영양소 수준이 아닌 제품 수준에서 수행되었습니다.

- 대상 영양소 유형 - 미량영양소: Zn, Mn, Cu, Fe, Mo, B 등

- 평균 영양소 적용률 - 국가별 농지 XNUMXha당 평균 영양소 소비량을 의미합니다.

- 적용되는 작물 유형 - 농작물: 곡물, 콩류, 유지 종자 및 섬유 작물 원예: 과일, 야채, 농장 작물 및 향신료, 잔디 및 관상용 작물

| 키워드 | 정의 |

|---|---|

| 무료 바카라 게임 | 영양요구량을 확보하기 위해 작물에 적용하는 화학물질로 과립, 분말, 액상, 수용성 등 다양한 형태로 제공됩니다. |

| 특수 무료 바카라 게임 | 토양, 잎, 무료 바카라 게임를 통해 적용되는 향상된 효율성과 영양분 가용성을 위해 사용됩니다. CRF, SRF, 액체무료 바카라 게임, 수용성무료 바카라 게임 등이 포함됩니다. |

| 제어 방출 무료 바카라 게임(CRF) | 폴리머, 폴리머-유황 및 수지와 같은 기타 재료로 코팅하여 전체 수명 주기 동안 작물의 영양분 가용성을 보장합니다. |

| 서방형 무료 바카라 게임(SRF) | 유황, 님나무 등과 같은 물질로 코팅하여 작물의 영양분 가용성을 장기간 보장합니다. |

| 잎 무료 바카라 게임 | 엽면 살포를 통해 적용되는 액체 및 수용성 무료 바카라 게임로 구성됩니다. |

| 수용성 무료 바카라 게임 | 액체, 분말 등 다양한 형태로 사용 가능하며 무료 바카라 게임 시비의 엽면 및 관비 모드에 사용됩니다. |

| 무료 바카라 게임 | 점적 관개, 미세 관개, 스프링클러 관개 등과 같은 다양한 관개 시스템을 통해 무료 바카라 게임를 적용합니다. |

| 무수 암모니아 | 무료 바카라 게임로 사용되며 토양에 직접 주입되며 기체 액체 형태로 제공됩니다. |

| 단일 슈퍼 인산염(SSP) | 인 함량이 35% 이하인 인만을 함유한 인무료 바카라 게임. |

| 삼중 슈퍼 인산염(TSP) | 인 함량이 35% 이상인 인무료 바카라 게임. |

| 향상된 효율성 무료 바카라 게임 | 다른 무료 바카라 게임에 비해 효율성을 높이기 위해 다양한 성분을 추가로 코팅하거나 처리한 무료 바카라 게임입니다. |

| 일반 무료 바카라 게임 | 살포, 줄타기, 쟁기질 토양 깔기 등 전통적인 방법으로 작물에 시비하는 무료 바카라 게임. |

| 킬레이트화 미량 영양소 | EDTA, EDDHA, DTPA, HEDTA 등과 같은 킬레이트제로 코팅된 미량 영양소 무료 바카라 게임 |

| 액체 무료 바카라 게임 | 액체 형태로 제공되며 주로 엽면 및 무료 바카라 게임를 통해 작물에 무료 바카라 게임를 적용하는 데 사용됩니다. |

시장 정의에 대한 자세한 내용이 필요하십니까?

질문하기

연구 방법론

바카라 사이트는 모든 바카라에서 XNUMX단계 방법론을 따릅니다.

- 1단계: 주요 변수 식별: 강력한 예측 방법론을 구축하기 위해 1단계에서 식별된 변수와 요인을 사용 가능한 과거 시장 수치와 비교하여 테스트합니다. 반복적인 과정을 통해 시장 예측에 필요한 변수를 설정하고 이를 기반으로 모델을 구축한다.

- 2단계: 시장 모델 구축: 예측 연도의 시장 규모 추정치는 명목 기준입니다. 인플레이션은 가격 책정의 일부가 아니며 평균 판매 가격(ASP)은 각 국가의 예측 기간 동안 일정하게 유지됩니다.

- 3단계: 확인 및 마무리: 이 중요한 단계에서 모든 시장 수치, 변수 및 분석가 호출은 연구 대상 시장의 주요 연구 전문가로 구성된 광범위한 네트워크를 통해 검증됩니다. 응답자는 연구 대상 시장의 전체론적 그림을 생성하기 위해 수준과 기능에 따라 선택됩니다.

- 4단계: 연구 산출물: 신디케이트 바카라, 맞춤형 컨설팅 과제, 데이터베이스 및 구독 플랫폼

연구 방법론에 대한 자세한 내용을 확인하세요

PDF 다운로드