South America Polycarbonate (에볼루션 바카라) Market Size and Share

시장 개관

| 학습 기간 | 2019 - 2030 |

| 산정기준연도 | 2024 |

| 예측 데이터 기간 | 2025 - 2030 |

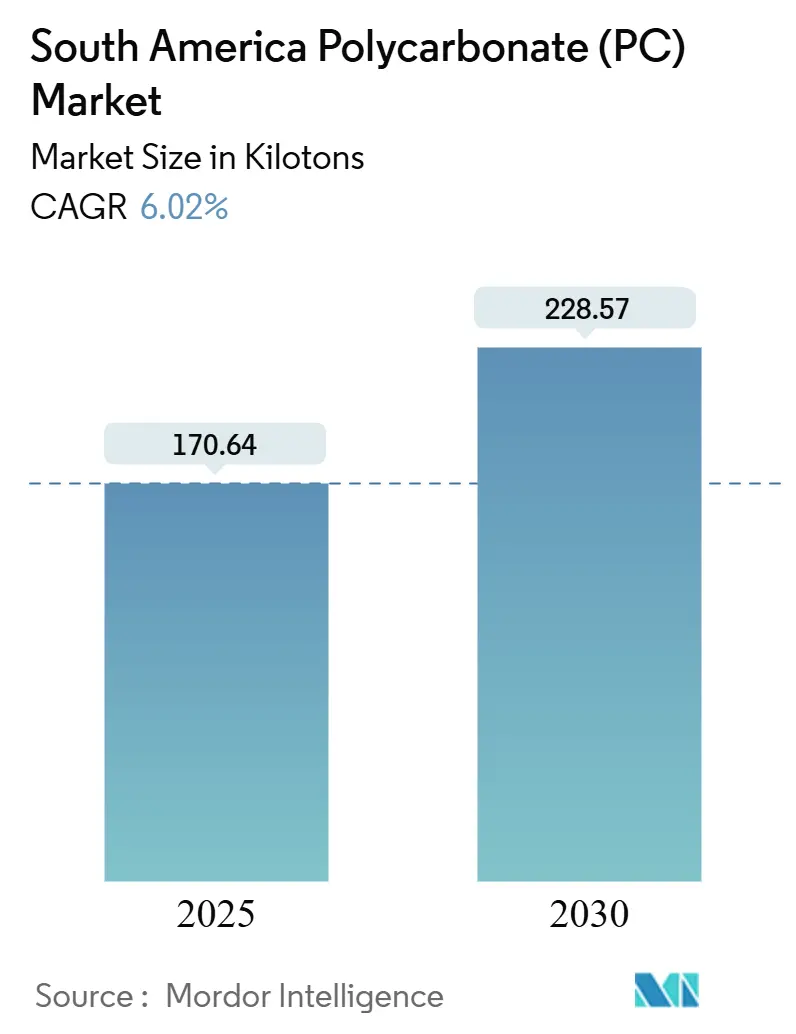

| 시장 규모(2025년) | 170.64 킬로 톤 |

| 시장 규모(2030년) | 228.57 킬로 톤 |

| 성장률(2025년~2030년) | 6.02 % CAGR |

| 시장 집중 | 높음 |

주요 선수

*면책조항: 주요 플레이어는 특별한 순서 없이 정렬되었습니다. 이미지 © 바카라 사이트. 재사용 시 CC BY 4.0에 따라 저작자 표시가 필요합니다. |

|

South America Polycarbonate (에볼루션 바카라) Market Analysis by 바카라 사이트

The South America Polycarbonate Market size is estimated at 170.64 kilotons in 2025, and is expected to reach 228.57 kilotons by 2030, at a CAGR of 6.02% during the forecast period (2025-2030). The outlook hinges on Brazil’s construction resurgence, Argentina’s automotive rebound, and the broader electrification of consumer devices, collectively widening end-use adoption. Manufacturers are shifting toward sustainable grades that incorporate recycled or bio-attributed content, responding to government carbon targets and procurement policies that reward low-carbon materials. Brazil continues to anchor supply with its large processing base and extensive distribution networks. At the same time, rising import tariffs on polymers, feedstock cost pressures linked to high natural gas prices, and evolving green building codes are reshaping competitive tactics. Regional players that align their portfolios with circular economy mandates and energy-efficient construction standards are poised to capture new specification wins across the forecast period.

주요 바카라 요약

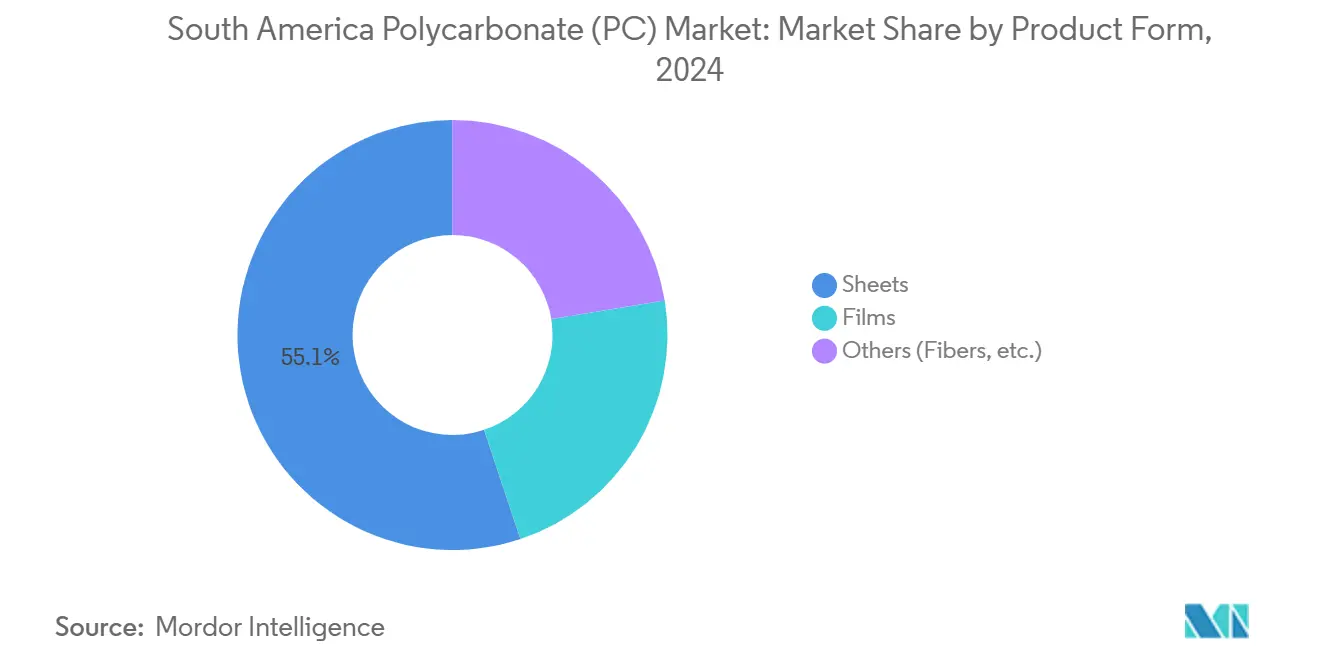

- By product form, sheets led with 55.12% of the South America polycarbonate market share in 2024. Films are projected to expand at a 6.53% CAGR through 2030.

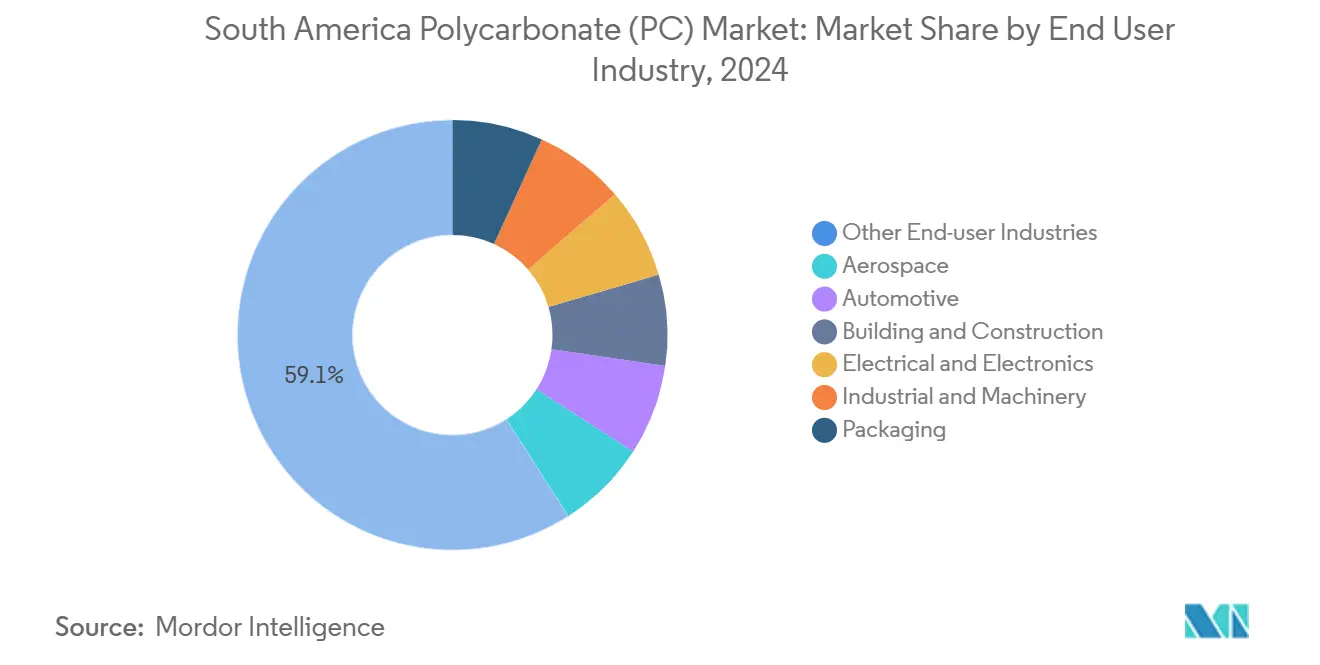

- By end-user industry, Other End-user Industries accounted for a 59.06% share of the South America polycarbonate market size in 2024. Electrical and Electronics is set to progress at a 6.84% CAGR to 2030.

- By geography, Brazil accounted for 40.66% of the South America polycarbonate market in 2024. Argentina is forecast to record a 6.60% CAGR from 2025-2030.

South America Polycarbonate (에볼루션 바카라) Market Trends and Insights

드라이버 영향 분석

| 드라이버 | (~) CAGR 예측에 미치는 영향 | 지리적 관련성 | 영향 타임라인 |

|---|---|---|---|

| EV-related lightweighting demand | 1.5% | Brazil and Argentina, spillover to the remaining countries | 중기(2~4년) |

| Electrification of electronics production | 2.0% | Concentrated in Brazil and Argentina | 단기 (≤ 2년) |

| Construction boom and green-building codes | 1.8% | Brazil dominant, Argentina and Chile secondary | 장기 (≥ 4년) |

| OEM use of paint-free high-gloss 에볼루션 바카라 | 1.2% | Brazil and Argentina automotive hubs | 중기(2~4년) |

| Uptake of recycled or bio-based 에볼루션 바카라 | 0.7% | Region-wide, early lead in Brazil | 중기(2~4년) |

출처: 모르도르 정보

Rising EV-Related Lightweighting Demand

Electric-vehicle production growth is driving increased demand for polycarbonate volumes in battery modules, lighting, and interior trim. Argentina aims to increase its production of assembled vehicles in 2025, which is expected to drive demand for lightweight components that enhance driving range. Brazilian assemblers specify impact-resistant grades for dashboards and charging stations that outperform traditional steel or aluminum in weight and processability. Government incentives that link tax relief to carbon-emission reductions reinforce polymer substitution in body parts and structural housings.

Electrification of Consumer-Electronics Production

Regional device manufacturers are turning to flame-retardant polycarbonate to meet UL 94 V-0 safety standards while retaining the freedom of thin-wall design. SABIC introduced LNP ELCRES CXL copolymers in December 2024 and January 2025, which enhance chemical resistance in smartphones, wearables, and chargers, highlighting how innovation addresses new form-factor needs[1]SABIC, “Press release: LNP ELCRES CXL polycarbonate copolymers,” sabic.com.

Construction Boom in Brazil and Green-Building Codes

Federal sustainability frameworks encourage daylighting and energy-efficient façades. Brazil’s PROCEL Edifica program lists polycarbonate glazing as an approved daylighting solution, and municipal programs such as Rio de Janeiro’s Qualiverde cut licensing fees for projects that adopt high-performance roofs and cladding. Energy-audited office buildings report 32-36% electricity savings after polycarbonate installation.

Shift Toward Recycled/Bio-Based 에볼루션 바카라 to Meet ESG Mandates

Corporate net-zero goals and ISO 14001 certifications elevate demand for circular grades. Discounted post-consumer pellets and Braskem’s target of 1 million tons of bio-based output by 2030 lower acquisition costs and carbon footprints, prompting converters to integrate recycled content into electronics and packaging lines.

제약 영향 분석

| 감금 | (~) CAGR 예측에 미치는 영향 | 지리적 관련성 | 영향 타임라인 |

|---|---|---|---|

| Bisphenol-A feedstock volatility | -1.2 % | Brazil and Argentina most exposed | 단기 (≤ 2년) |

| Import dependence for specialty grades | -0.8 % | Brazil primary, Argentina secondary | 중기(2~4년) |

| Lagging recycling infrastructure | -0.6 % | 지역 전체, 소규모 경제권에서 급성 | 장기 (≥ 4년) |

출처: 모르도르 정보

Bisphenol-A Feedstock Price Volatility

Lower operating rates in Asia swing global BPA prices and erode South American converter margins. The pinch is amplified by Brazilian natural-gas costs, which are above levelized U.S. or Asian rates near USD 2, making local polymerization less competitive.

Import Dependence for Specialty Grades

Brazil’s 20% import tariff on polymers enacted in 2024 inflates landed costs for flame-retardant or optical-grade polycarbonate that lacks domestic production. Extended lead times and currency swings compound planning risk for downstream molders.

세그먼트 분석

By Product Form: Sheets Anchor Demand

Polycarbonate sheets held 55.12% of South America's polycarbonate market share in 2024 on the back of roofing, glazing, and signage applications in rapidly urbanizing corridors. The South America polycarbonate market size for sheets benefits from municipal tax incentives that rate daylight-harvesting façades as energy-saving investments. Films, posting a 6.53% CAGR, gain momentum in protective electronics packaging and optical media. Corrugated, solid, and multi-wall sheet designs enable architects to reduce HVAC loads while meeting increasingly stringent thermal insulation targets. Argentina’s auto assemblers have begun sourcing thin-gauge sheets for interior consoles, a shift that foreshadows incremental tonnage gains once full EV production scales.

Long-run competitiveness in sheets hinges on extrusion efficiency and resin sourcing strategies. Producers that combine in-house recycling streams with bio-attributed feedstock can capture price premiums from developers pursuing green-building certification points. Film fabricators require tighter process control and often cluster near Brazil’s electronics hubs, where localized supply slashes transit times and scrap rates. Specialty fibers remain niche in aerospace and safety glazing but deliver high margins through customized modulus and flame-retardant packages.

참고: 바카라 구매 시 사용 가능한 모든 개별 세그먼트의 세그먼트 공유

By End-User Industry: Electronics Outpaces Aggregate Growth

Other End-user Industries comprised 59.06% of the 2024 volume as polycarbonate pervades industrial machinery, aerospace fairings, and rigid-wall packaging. Electrical and Electronics, however, outstrips the aggregate at a 6.84% CAGR. Smartphone casings, LED lenses, and power-supply housings value the dielectric strength and dimensional stability that virgin or recycled polycarbonate provides, eliminating the need for metal stamping costs. The South American polycarbonate market size for electronics reflects the rising regional EMS (electronics manufacturing services) capacity that supports local smartphone and appliance demand. The automotive industry continues its climb toward lightweighting, yet the largest short-term accelerator remains stringent flammability norms in data centers and e-mobility chargers.

Segment diversification is reinforced by supplier innovation. SABIC’s 2025 LNP ELCRES CXL line and Covestro’s high-에볼루션 바카라R resins provide OEM design teams with fresh options to meet optical, color, and regulatory targets simultaneously[2]Covestro, “Investors update 2025,” covestro.com. The adoption pace hinges on converters equipping lines with halogen-free flame-retardant compounding and color-match laboratories that ensure part consistency across multi-site programs.

참고: 바카라 구매 시 사용 가능한 모든 개별 세그먼트의 세그먼트 공유

지리 분석

Brazil captured 40.66% of 2024 demand due to its broad polycarbonate processing ecosystem and building-code incentives that promote energy-efficient skylights and canopies. National policies are now piloting tax rebates for façades that reduce operational emissions, which boosts sheet uptake in commercial retrofits. However, domestic producers wrestle with feedstock cost penalties linked to elevated natural-gas tariffs, a factor that intensifies reliance on imported specialty resins despite higher duties. Braskem’s push for bio-polymer production, aiming for 1 million tons by 2030, could rebalance the supply chain if bio-based precursors achieve cost parity.

Argentina is the fastest-growing buyer, with a 6.60% CAGR through 2030. Automotive assembly rebounds around Córdoba and Rosario, and public procurement frameworks targeting electric bus fleets boost demand for high-impact polycarbonate glazing and battery housings. The country’s Vaca Muerta shale play offers potential feedstock relief once pipeline and cracker projects mature, but until then, import streams dominate.

The rest of South America, encompassing Chile, Colombia, Peru, and smaller economies, adds moderate incremental tonnage. Mining operations in Chile utilize abrasion-resistant polycarbonate guards and covers, whereas Colombia’s aerospace cluster employs ballistic-grade sheets in its defense platforms.

경쟁 구도

Global majors maintain durable positions through application engineering support and multipurpose distribution hubs in São Paulo and Buenos Aires. The South America polycarbonate market is consolidated. Regional players specialize in compounding and color matching for domestic appliance brands, thereby gaining agility on smaller production runs.

Tariff shifts and high logistics costs nudge some processors to explore localized polymerization, yet feedstock disadvantages limit scale. Players that form feedstock alliances with ethanol-to-ethylene ventures or invest in mechanical recycling upgrades can protect margins while serving emerging green procurement lists from multinationals. Strategic partnerships seek to secure renewable monomer streams that underpin future automotive and electronics specifications.

South America Polycarbonate (에볼루션 바카라) Industry Leaders

-

SABIC

-

코 베스트로 AG

-

LG 화학

-

미쓰비시 화학 그룹 주식회사

-

테이 진 리미티드

- *면책조항: 주요 플레이어는 특별한 순서 없이 정렬되었습니다.

최근 산업 발전

- January 2025: SABIC launched LNP ELCRES CXL copolymers offering upgraded chemical resistance for mobility, electronics, and industrial uses.

- May 2024: Covestro AG released a polycarbonate resin with 90% post-consumer recycled content that achieves UL 94 V-0 at 1.5 mm and delivers a 70% lower carbon footprint than virgin resin.

이 바카라를 사용하면 무료

우리는 업계의 기본 구조를 나타내는 글로벌 및 지역 지표에 대한 포괄적이고 포괄적인 데이터 포인트 세트를 무료로 제공합니다. 15개 이상의 무료 차트 형식으로 제공되는 이 섹션에서는 승용차 생산, 상용차 생산, 오토바이 생산, 항공우주 부품 생산, 전기 및 전자 제품 생산, 엔지니어링 플라스틱 수요에 대한 지역 데이터 등 다양한 최종 사용자 생산 동향에 대한 희귀한 데이터를 다룹니다. 등.

표 및 그림 목록

- 그림 1 :

- 항공우주 부품 생산 수익, USD, 남아메리카, 2017 - 2029

- 그림 2 :

- 2017년부터 2029년까지 남아메리카의 자동차, 단위 생산량

- 그림 3 :

- 신축 건물의 바닥 면적, 평방 피트, 남아메리카, 2017 - 2029

- 그림 4 :

- 전기 및 전자 제품의 생산 수익, USD, 남아메리카, 2017 - 2029

- 그림 5 :

- 남아메리카, 2017년 - 2029년 플라스틱 포장 생산량, 톤수

- 그림 6 :

- 남아메리카 상위 국가별 에볼루션 바카라(PC) 무역 수입 수익, USD, 2017-2021

- 그림 7 :

- 남아메리카 상위 국가별 에볼루션 바카라(PC) 무역의 수출 수익, 2017-2021

- 그림 8 :

- 남미 에볼루션 바카라(PC) 시장, 가격 동향, 국가별, KG당 USD, 2017-2021년

- 그림 9 :

- 에볼루션 바카라(PC) 수익, 형태별, USD, 남미, 2017, 2023, 2029

- 그림 10 :

- 남아메리카, 2017년 - 2029년 에볼루션 바카라(PC) 소비량, 톤수

- 그림 11 :

- 남아메리카, 미국 달러 소비된 에볼루션 바카라(PC)의 가치, 2017년 - 2029년

- 그림 12 :

- 2017년부터 2029년까지 남아메리카 최종 사용자 산업에서 소비되는 에볼루션 바카라(PC)의 양, 톤

- 그림 13 :

- 최종 사용자 산업이 소비하는 에볼루션 바카라(PC)의 가치, 미국 달러, 남아메리카, 2017년 - 2029년

- 그림 14 :

- 최종 사용자 산업이 소비하는 에볼루션 바카라(PC)의 양적 점유율, %, 남아메리카, 2017년, 2023년, 2029년

- 그림 15 :

- 최종 사용자 산업이 소비하는 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2017년, 2023년, 2029년

- 그림 16 :

- 항공우주 산업에서 소비되는 폴리탄산염(에볼루션 바카라)의 양, 톤, 남아메리카, 2017년 - 2029년

- 그림 17 :

- 항공우주 산업에서 소비되는 에볼루션 바카라(PC)의 가치, 미국 달러, 남아메리카, 2017년 - 2029년

- 그림 18 :

- 항공우주 산업에서 소비되는 국가별 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 19 :

- 자동차 산업에서 소비되는 에볼루션 바카라(PC)의 양, 톤, 남아메리카, 2017년 - 2029년

- 그림 20 :

- 자동차 산업에서 소비되는 에볼루션 바카라(PC)의 가치, 미국 달러, 2017년 - 2029년

- 그림 21 :

- 자동차 산업에서 소비되는 국가별 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 22 :

- 건축 및 건설 산업에서 소비되는 에볼루션 바카라(PC)의 양, 톤, 남아메리카, 2017년 - 2029년

- 그림 23 :

- 건축 및 건설 산업에서 소비되는 에볼루션 바카라(PC)의 가치, 미국 달러, 남아메리카, 2017 - 2029

- 그림 24 :

- 국가별 건축 및 건설 산업에서 소비되는 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 25 :

- 전기 및 전자 산업에서 소비되는 폴리탄산염(에볼루션 바카라)의 양, 톤, 남아메리카, 2017년 - 2029년

- 그림 26 :

- 전기 및 전자 산업에서 소비되는 폴리탄산염(에볼루션 바카라)의 가치, 미국 달러, 남아메리카, 2017년 - 2029년

- 그림 27 :

- 국가별 전기 및 전자 산업에서 소비되는 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 28 :

- 산업 및 기계 산업에서 소비되는 폴리탄산염(에볼루션 바카라)의 양, 톤, 남아메리카, 2017년 - 2029년

- 그림 29 :

- 산업 및 기계 산업에서 소비되는 에볼루션 바카라(PC)의 가치, 미국 달러, 남아메리카, 2017 - 2029

- 그림 30 :

- 국가별 산업 및 기계 산업에서 소비되는 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 31 :

- 포장 산업에서 소비되는 에볼루션 바카라(PC)의 양, 톤, 남아메리카, 2017년 - 2029년

- 그림 32 :

- 포장 산업에서 소비되는 에볼루션 바카라(PC)의 가치, 미국 달러, 2017년 - 2029년

- 그림 33 :

- 국가별 포장 산업에서 소비되는 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 34 :

- 기타 최종 사용자 산업에서 소비되는 에볼루션 바카라(PC)의 양, 남아메리카, 2017년 - 2029년

- 그림 35 :

- 기타 최종 사용자 산업에서 소비되는 에볼루션 바카라(PC)의 가치, 미국 달러, 남아메리카, 2017년 - 2029년

- 그림 36 :

- 기타 최종 사용자 산업에서 소비되는 에볼루션 바카라(PC)의 국가별 가치 점유율, %, 남아메리카, 2022년 VS 2029년

- 그림 37 :

- 2017년부터 2029년까지 남아메리카 국가별 소비된 폴리탄산염(에볼루션 바카라)의 양, 톤수

- 그림 38 :

- 남아메리카 국가별 소비되는 에볼루션 바카라(PC)의 가치, 2017년 - 2029년

- 그림 39 :

- 국가별 에볼루션 바카라(PC) 소비량 비율, %, 남아메리카, 2017년, 2023년, 2029년

- 그림 40 :

- 국가별 에볼루션 바카라(PC) 소비량 비율, %, 남아메리카, 2017년, 2023년, 2029년

- 그림 41 :

- 폴리탄산염(에볼루션 바카라) 소비량, 톤, 아르헨티나, 2017년 - 2029년

- 그림 42 :

- 소비된 에볼루션 바카라(PC)의 가치, USD, 아르헨티나, 2017 - 2029

- 그림 43 :

- 최종 사용자 산업이 소비하는 에볼루션 바카라(PC)의 가치 점유율, %, 아르헨티나, 2022년 VS 2029년

- 그림 44 :

- 2017년부터 2029년까지 브라질, 폴리탄산염(에볼루션 바카라) 소비량, 톤수

- 그림 45 :

- 에볼루션 바카라(PC) 소비량, 미국 달러, 브라질, 2017년 - 2029년

- 그림 46 :

- 최종 사용자 산업이 소비하는 에볼루션 바카라(PC)의 가치 점유율, %, 브라질, 2022년 VS 2029년

- 그림 47 :

- 2017년 - 2029년 남아메리카 기타 지역의 폴리탄산염(에볼루션 바카라) 소비량, 톤수

- 그림 48 :

- 소비된 에볼루션 바카라(PC)의 가치, 미국 달러, 남아메리카 기타 지역, 2017년 - 2029년

- 그림 49 :

- 최종 사용자 산업이 소비하는 에볼루션 바카라(PC)의 가치 점유율, %, 남아메리카 나머지 지역, 2022년 VS 2029년

- 그림 50 :

- 전략적 움직임 수 기준 가장 활동적인 기업, 남아메리카, 2019~2021

- 그림 51 :

- 가장 많이 채택된 전략, COUNT, 남미, 2019 - 2021

- 그림 52 :

- 주요 업체별 에볼루션 바카라(PC) 수익 점유율, %, 남아메리카, 2022

South America Polycarbonate (에볼루션 바카라) Market Report Scope

항공우주, 자동차, 건축 및 건설, 전기 및 전자, 에볼루션 바카라 및 기계, 포장은 최종 사용자 에볼루션 바카라별로 세그먼트로 다루어집니다. 아르헨티나, 브라질은 국가별로 세그먼트로 다루어집니다.| 제품 형태별 | 시트 |

| 영화 | |

| 기타(섬유 등) | |

| 최종 사용자 산업별 | Aerospace |

| 자동차 | |

| 건축 및 건설 | |

| 전기 전자 | |

| 산업 및 기계 | |

| 포장 | |

| 기타 최종 사용자 에볼루션 바카라 | |

| 지리학 | Brazil |

| Argentina | |

| 남아메리카의 나머지 지역 |

| 시트 |

| 영화 |

| 기타(섬유 등) |

| Aerospace |

| 자동차 |

| 건축 및 건설 |

| 전기 전자 |

| 산업 및 기계 |

| 포장 |

| 기타 최종 사용자 에볼루션 바카라 |

| Brazil |

| Argentina |

| 남아메리카의 나머지 지역 |

시장 정의

- 최종 사용자 에볼루션 바카라 - 건축 및 건설, 포장, 자동차, 항공 우주, 산업 기계, 전기 및 전자 및 기타는 에볼루션 바카라 시장에서 고려되는 최종 사용자 산업입니다.

- 수지 - 연구 범위 내에서 분말, 과립 등과 같은 XNUMX차 형태의 버진 에볼루션 바카라 수지가 고려됩니다.

| 키워드 | 정의 |

|---|---|

| 아세탈 | 표면이 미끄러운 단단한 소재입니다. 가혹한 작업 환경에서도 마모와 손상을 쉽게 견딜 수 있습니다. 이 에볼루션 바카라머는 기어, 베어링, 밸브 부품 등과 같은 건축 응용 분야에 사용됩니다. |

| 아크릴 | 이 합성수지는 아크릴산의 유도체입니다. 매끄러운 표면을 형성하며 주로 실내의 다양한 용도로 사용됩니다. 이 소재는 특수 배합으로 옥외용으로도 사용할 수 있습니다. |

| 캐스트 필름 | 캐스트 필름은 표면에 플라스틱 층을 증착한 다음 해당 표면에서 필름을 굳히고 제거하여 만들어집니다. 플라스틱 층은 용융된 형태, 용액 또는 분산 형태일 수 있습니다. |

| 착색제 및 안료 | 착색제 및 안료는 플라스틱의 색상을 변경하는 데 사용되는 첨가제입니다. 분말 또는 수지/색상 프리믹스일 수 있습니다. |

| 복합 재료 | 복합재료는 두 개 이상의 구성재료로 만들어진 재료이다. 이러한 구성 재료는 서로 다른 화학적 또는 물리적 특성을 가지며 병합되어 개별 요소와 다른 특성을 가진 재료를 만듭니다. |

| 중합도(DP) | 거대분자, 중합체 또는 올리고머 분자의 단량체 단위 수를 중합도 또는 DP라고 합니다. 유용한 물리적 특성을 지닌 플라스틱은 종종 수천 개의 DP를 갖습니다. |

| 분산 | 다른 물질에 물질의 현탁액 또는 용액을 생성하려면 한 물질의 미세하고 응집된 고체 입자를 액체나 다른 물질에 분산시켜 분산액을 형성합니다. |

| 유리 섬유 | 유리섬유 강화 플라스틱은 수지 매트릭스에 유리섬유가 내장되어 구성된 소재입니다. 이 재료는 인장강도와 충격강도가 높습니다. 난간과 플랫폼은 표준 유리섬유를 사용하는 경량 구조 응용 분야의 두 가지 예입니다. |

| 섬유 강화 에볼루션 바카라머(FRP) | 섬유 강화 에볼루션 바카라머는 섬유로 강화된 에볼루션 바카라머 매트릭스로 만들어진 복합 재료입니다. 섬유는 일반적으로 유리, 탄소, 아라미드 또는 현무암입니다. |

| 플레이크 | 이는 일반적으로 표면이 고르지 않은 건조하고 벗겨진 조각으로, 셀룰로오스 플라스틱의 기초입니다. |

| 플루오로 에볼루션 바카라머 | 이는 다중 탄소-불소 결합을 갖는 플루오로카본 기반 에볼루션 바카라머입니다. 이는 용매, 산 및 염기에 대한 높은 저항성을 특징으로 합니다. 이러한 재료는 단단하면서도 기계 가공이 쉽습니다. 널리 사용되는 불소 중합체로는 PTFE, ETFE, PVDF, PVF 등이 있습니다. |

| 케블라 | Kevlar는 처음에는 Dupont의 아라미드 섬유 브랜드였던 아라미드 섬유의 일반적 이름입니다. 섬유, 필라멘트 또는 시트로 만들어진 경량, 내열성, 고체, 합성, 방향족 에볼루션 바카라아미드 소재 그룹을 아라미드 섬유라고 합니다. 파라아라미드와 메타아라미드로 분류됩니다. |

| 얇은 판 모양의 | 원하는 모양과 너비를 만들기 위해 압력과 열로 결합된 연속적인 재료 층으로 구성된 구조 또는 표면입니다. |

| 나일론 | 이는 실과 모노필라멘트로 형성된 합성 섬유 형성 에볼루션 바카라아미드입니다. 이 섬유는 인장강도, 내구성, 탄력성이 뛰어납니다. 녹는점이 높고 화학 물질과 다양한 액체에 저항할 수 있습니다. |

| PET 프리폼 | 프리폼은 에볼루션 바카라에틸렌 테레프탈레이트(PET) 병이나 용기에 주입되는 중간 제품입니다. |

| 플라스틱 배합 | 컴파운딩은 원하는 특성을 달성하기 위해 용융 상태의 에볼루션 바카라머와 첨가제를 혼합 및/또는 혼합하여 플라스틱 제제를 준비하는 것으로 구성됩니다. 이러한 혼합물은 일반적으로 피더/호퍼를 통해 고정된 설정값으로 자동 투입됩니다. |

| 플라스틱 펠렛 | 사전 생산 펠릿 또는 너들이라고도 알려진 플라스틱 펠렛은 플라스틱으로 만들어진 거의 모든 제품의 구성 요소입니다. |

| 중합 | 이는 여러 단량체 분자가 안정적인 공유 결합을 형성하는 중합체 사슬을 형성하는 화학 반응입니다. |

| 스티렌 공중합체 | 공중합체는 한 가지 이상의 단량체 종에서 파생된 중합체이고, 스티렌 공중합체는 스티렌과 아크릴레이트로 구성된 중합체 사슬입니다. |

| 열가소성 수지 | 열가소성 플라스틱은 가열하면 부드러워지고 냉각되면 단단해지는 고분자로 정의됩니다. 열가소성 수지는 광범위한 특성을 갖고 있으며 물리적 특성에 영향을 주지 않고 재성형 및 재활용이 가능합니다. |

| 버진 플라스틱 | 한 번도 사용, 가공, 개발된 적이 없는 플라스틱의 기본 형태입니다. 재활용되거나 이미 사용된 재료보다 더 가치 있는 것으로 간주될 수 있습니다. |

연구 방법론

바카라 사이트는 모든 바카라에서 XNUMX단계 방법론을 따릅니다.

- 1단계: 주요 변수 식별: 특정 제품 부문 및 국가와 관련된 정량화 가능한 주요 변수(에볼루션 바카라 및 외부)는 탁상 조사 및 문헌 검토를 기반으로 관련 변수 및 요인 그룹에서 선택됩니다. 기본 전문가 입력과 함께. 이러한 변수는 회귀 모델링(필요할 때마다)을 통해 추가로 확인됩니다.

- 2단계: 시장 모델 구축: 강력한 예측 방법론을 구축하기 위해 1단계에서 식별된 변수와 요인을 사용 가능한 과거 시장 수치와 비교하여 테스트합니다. 반복적인 과정을 통해 시장 예측에 필요한 변수를 설정하고 이를 기반으로 모델을 구축한다.

- 3단계: 확인 및 마무리: 이 중요한 단계에서 모든 시장 수치, 변수 및 분석가 호출은 연구 대상 시장의 주요 연구 전문가로 구성된 광범위한 네트워크를 통해 검증됩니다. 응답자는 연구 대상 시장의 전체론적 그림을 생성하기 위해 수준과 기능에 따라 선택됩니다.

- 4단계: 연구 산출물: 신디케이트 바카라, 맞춤형 컨설팅 과제, 데이터베이스 및 구독 플랫폼